Introspective

Business World, 25 September 2017

Once upon a time, I was a co-panelist of Mr. Ronnie Concepcion in a program hosted by Ms. Kris Aquino. I don’t remember what transpired during the televised discussion but vivid in my memory was my brief exchange with Ronnie before we faced the camera. I introduced myself to Mr. Concepcion as from the UP School of Economics. He immediately observed that the problem with the UP School of Economics was that it did not understand protection of domestic industries. The policy debate of the day, if memory serves me right, was trade liberalization and the lifting of trade barriers, which many economists and the World Bank favored, but opposed by the PCCI and other trade groups. My position at that time differed in a small way from the orthodoxy of just lifting tariff and quotas. I simply stated, “But I am a protectionist!” This took Ronnie aback. “How come, when you want to open domestic industries to unfair foreign competition?”

I said, “I am a protectionist. I want to use a weak peso to protect domestic industries.” Ronnie, I understood, wanted to use tariff and quotas to protect domestic industries.

The difference between us was? and is? the instrument, not the sentiment. But what a whale of a difference! Tariffs and quotas protect domestic industries in Manila, Cebu, and Davao. A weak peso protects domestic industries in Manila, Cebu, and Davao but, on top of that, also in London, Paris, and San Francisco. It is protection without borders. Tariffs and quotas encourage smuggling; especially since Mr. Concepcion also defended the strong peso to render imported inputs cheap; a weak peso discourages smuggling!

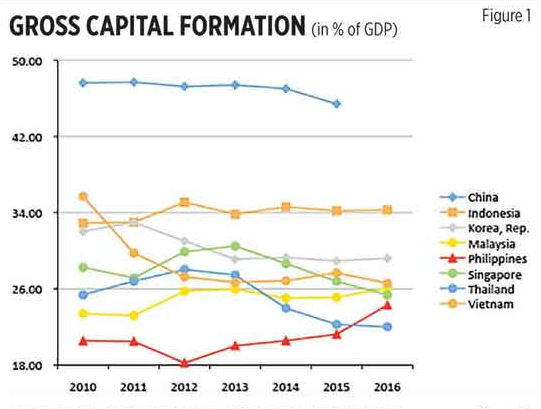

This difference produced the crack that would become a chasm between the fast fading Philippines and the emerging East Asian Miracle economies who thrived on manufactured export growth and the high investment rate it sustained (between 25%-40%). The Philippines in contrast became inward-looking, retreated to primary products for export earnings (lumber, sugar, nickel, and coconut) and turned to the Services sector for growth. The dynamism of the Service sector is always self-limited by the boom and bust cycles and the BoP crises it sets in motion. The Philippines entered the era of investment compression, when a 2.5% government capital outlay and a 20% investment rate was normal. (Figure 1 gives the comparative investment rates from 2010 to 2016). The Philippines’ trajectory is in red and hovered around a dismal 20% (see Figure 1).

Competitiveness in tatters, we turned to exporting excess labor to foreign countries and to the murky world of informal sector. We became dependent on OFW remittance which is now being threatened by excess capacity in global oil. Furthermore, the artificial intelligence technology threatens to overturn our BPO applecart.

The investment-led growth as operationalized by the Duterte administration means a Government Capital Outlay (GCO) racing to 8% by the end of Duterte’s term up from the long-term average of 2.5% of GDP. The much-maligned Aquino Administration had managed to raise the investment rate to 24%, a level not reached since the 1980s. An investment rate of 25%+ would put the Philippines at the doorstep of investment-driven economies; it will not close the gap with our rivals unless we push it farther to tiger economies’ standard of 30%-35%. Still and all, investment decompression is sine qua non for exit from the rut.

In an investment-led growth, domestic output tends to outpace domestic demand which threatens supply gluts. In a closed economy, these gluts will cause overall recession (economic busts) and the high investment regime withers. In an open economy, the excess supply of Tradables (T) can find markets abroad while no such recourse exists for the excess supply of Non-tradables (NTs). The glut in NTs will induce price declines of NT. There is a real depreciation.

But it is sustainability of investment-led growth that matters.

In an open economy, the investment-led growth can be sustained by the buoyancy in T. Prominent observers Young, Krugman, and Collins and Bosworth all fingered capital accumulation as under-girders of rapid growth of East Asian Tigers which, you guessed it, was sustained by high export growth. Sustained growth means South Korea growing at 8% on average annually from 1960 to 1994. The investment-led growth creates its own export bias which in turn sustains the high investment rates.

Lately, the gradual depreciation of the peso (to P51/$) was accompanied by the familiar angst in the media. Figure 2 below, borrowed from Dr. Victor Abola, shows that indeed the nominal depreciation of the peso in 2017 (above 100 and in red) has exceeded that of its Asian rivals (see Figure 2).

This development is not new. What is new? This is happening without the familiar war frenzy among the authorities; there seems instead a healthy nonchalance (e.g., BusinessWorld, 22 July 2017). Wholly understandable because benefitting a larger more important constituency victimized by the strong peso (OFW, BPO, and export-oriented PEZA locators). This weakening itself could result from baby steps towards an investment-led growth. The share of capital imports and imported input combined in total imports together exceeded 70% of total and the investment rate exceeded 24% in 2016 up from customary 20% (see Figure 1).

Though heart-warmed, this dismal scientist wants more assurance. We were once at P55/$ during the Asian Financial Crisis but past BSP dragged it down to P40/$. Wasted opportunity! The Chinese do not waste such opportunity. After the devaluing the yuan 40% in 1994, PRC fixed the imbedded export bias for two decades and counting over widespread global protests. Those two-and-a-half decades saw an economic transformation unparalleled in history.

To work its magic, peso weakening must be sustained. The long-entrenched import bias in the currency must be truly exorcized. The reason is hysteresis, a phenomenon familiar to exact scientists. Hysteresis means when an import bias (alias overvaluation of the currency) of x% has built up an import orientation in the economy, it takes more than a x% depreciation (alias undervaluation) of the currency and one sustained for a long period to reverse the orientation. Nonlinearity is of the essence here; history matters.

Finally, if we want to reap the harvest of the high investment rate and BUILDx3, we need a sustained export bias to sustain the high investment rate. Rather than fear, we must embrace the weak peso!

Dr. Raul V. Fabella is a retired professor of the UP School of Economics and a member of National Academy of Science and Technology (NAST). He gets his dopamine fix from tennis, bicycling, and working the guitar where he spells rank amateurism. Weaving ideas in coffee shops is an integral part of his day.